A history of unusual payments at Ibrox

21/08/2017

This blog spent its first phase in 2011 and 2012 trying to draw attention to payments made to footballers by Rangers FC. All of those payments, Wee Tax case and Big Tax Case, have now been established to have involved the deliberate non-payment of taxes and lying to HMRC & the Scottish football authorities about the existence of side-contracts detailing those payments. However, these were not the only irregular-looking payments made by Rangers through the Murray Group Management Remuneration Trust (MGMRT).

If you will indulge me, and follow along closely, you will see that a clear pattern of behaviour emerges. This is yet another case where the devil is in the details. So forgive me for a long and very detailed post, but I hope it will be worth your time.

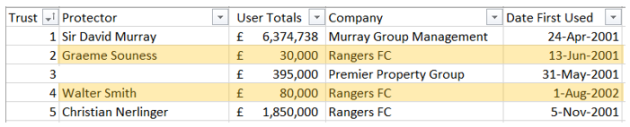

The following table shows the first five MGMRT sub-trust recipients, the number of their sub-trust, and the date the sub-trust was first used.

(I have chosen to obscure the name of the recipient of trust number 3 as he has no relevance to the Rangers story).

The sharp-eyed amongst you will notice something odd in the dates of first use for Messrs. Souness and Smith. At the First Tier Tribunal (FTT) in 2010-2012 the process of creating sub-trusts and allocating numbers was described in quite some depth. As an example, the following is an extract from Murray Group’s Ian MacMillan’s cross-examination on 26th October 2010:

This establishes the point that sub-trust numbers were allocated in time-sequenced order, one after the other as needed. Indeed, of the 111 sub-trusts created for the MGMRT all of the other 109 sub-trusts follow this format i.e. the order of sub-trust numbers lines up with the order of creation and first use i.e. sub-trust 5 was created before sub-trust 6 and so on. The only sub-trusts that do not appear to follow this pattern were those created for Souness and Smith.

Are you still with me? Hold on- we are about to get to the point. (A pen and paper to track the timeline might be useful!)

Why does Mr. Souness have sub-trust number 2 when his loan request was made on 13th June 2001- which is after the first use of sub-trust number 3 on 31st May 2001? Mr. Souness has said this payment was for scouting work performed for Rangers. Of course this was an odd response given that he was the manager of Blackburn Rovers at the time. Some cynics have suggested that the transfer of Tugay Kerimoğlu from Rangers to Mr. Souness’ Blackburn Rovers on 17th of May 2001 might be a related factor. A decision to open a sub-trust for Mr. Souness on or around the 17th of May 2001 would explain why he would be allocated sub-trust number 2. (Of course, there may be other explanations). Whatever the truth behind this payment to Souness, I think we can all agree that it is highly unusual for one club to make payments to a ‘long-since’ ex-employee who was working for another football club at the time.

Walter Smith’s sub-trust number 4 is even more perplexing. Funding of this trust took place in September 2002 based on a “loan request” letter submitted in early August 2002. This is unusual because we would expect, naturally, that sub-trust number 4 would be opened after sub-trust number 3 and before sub-trust number 5. Therefore, we would expect that the decision to open Mr. Smith’s sub-trust number 4 would have taken place between 31st May and the 5th of November 2001. This apparent delay in funding the sub-trust for Mr. Smith after having a number allocated is highly unusual in the context of the timeliness for the other Rangers sub-trusts. Those cynics might again wonder aloud if there was a connection between Michael Ball’s transfer from Everton to Rangers on 2nd August 2001 or Walter Smith’s termination as manager of Everton on 13th March 2002. A decision to open sub-trust number 4 for Walter Smith on or around 2nd August 2001 for Ball’s transfer would certainly fit the numbering of the sub-trusts perfectly. If this was the case, we would have a second case of Rangers making a payment to a ‘long-since’ former employee who was then the manager of a different club. (As background colour we might want to recall that in August 2001 Michael Ball was a rising star who had just received his first England cap. That his career did not take off at Ibrox was not something anyone would have anticipated in 2001).

Should we start to think once was a mistake, twice is just careless? Was funding delayed to wait until Smith was no longer the manager of another club? Of course, there may be many other explanations for this sequence of events. This blog post makes no accusations. It merely posits questions against data that comes from the Scottish Courts and Tribunals Service.

For the record, I am not aware of anyone asking Mr. Smith about his EBT. As mentioned above, tribunal documentation indicates that a “loan request” was made in Walter Smith’s name in August 2002 for £80,000 and the sub-trust was funded with this amount by Rangers on 24th September 2002. At the FTT Smith’s sub-trust was reported just like any other with no mention made of him not being paid. The submission excerpt above was originally interpreted by me as implying Smith did not withdraw the money, but I have received other information along the years that indicates that he did. I do not know for certain that he did. Someone should ask him. I will be pleased to provide any updates or corrections to this posting if Mr. Smith would like to provide more information.

However, it is not really important whether Walter Smith transferred this money or not. It is far more important that the many questions surrounding why Rangers were making payments to ex-employees get answered.

Could someone ask the SFA’s Andrew Dickson, who administered Rangers’ payments to sub-trusts, to explain the many questions raised by the timeline of these events? After all Mr. Dickson received an email from Ian MacMillan on 16th July 2002 asking him to look into why Smith had not had not been paid the agreed £80,000 by then. See excerpt from FTT submission below:

This reads like the agreement to pay Walter Smith this was made much earlier than 16 July 2002. Obviously, Mr. Smith will know what happened, but it is especially important that a man still involved in the administration of Scottish football for the SFA should explain what did he know about the Smith payment and what did he do with that information. “Mr. Dickson, did you ask anyone at Rangers or the Murray Group why the club was making payments to coach(es) of other club(s)? If not, why not? You were certainly aware that such payments had been made.”

When we add these events to the Wee Tax Case, the Big Tax Case, lying for years about the existence of side-letters, shredding of evidence of a contractual obligation, bilking Everton out of at least part of the transfer fee for the re-sale of Michael Ball, lying about the date of crystallisation of the Wee Tax Case bill- there is a pattern that emerges. There are prima facie fraud cases awaiting at least some of these events. It is blindingly obvious. Yet neither the Scottish Football Association nor the Scottish Professional Football League appear to “have any appetite” for investigating let alone addressing what was very clearly a major problem in the Scottish game. Many of the people who have serious questions to answer about this pattern are still in positions of authority within the Scottish game. What else did the men who ruined Rangers get up to? There can be no sense that Scottish football is fairly or competently administered while this pattern of unusual activity over many years goes uninvestigated.